In recent years, pension auto enrolment has become an essential responsibility for hundreds of thousands of business owners across the UK.

In this guide, we explain how auto enrolment works and what it means for your business if you have employees.

We also explain why sole traders and many small limited companies are exempt.

What is automatic enrolment?

Automatic enrolment is the UK’s mandatory workplace pension system.

All employers who fall within the scope of the rules must automatically enrol eligible workers into a workplace pension scheme and make minimum pension contributions on their behalf.

You can find out more about how it works on GOV.UK.

Which businesses are affected?

The automatic enrolment rollout began in October 2012 for larger firms. Since February 2018, all employers, including those with a single employee, have been required to comply with the legislation.

Even new employers, including those who started trading after 2017, must comply with AE duties from the first day they hire their first employee.

What if you don’t have any staff?

The rules don’t apply to sole traders (by definition). They also don’t apply if you run a limited company, and the following apply:

- You are the sole director of a limited company with no employees.

- Your limited company has two or more directors, no other employees, and neither director has a contract of employment.

- Your limited company has two or more directors, no other employees, and only one director is employed under a contract of employment.

- Your company has been dissolved, entered into liquidation, or ceased trading.

For more details on director exemptions, see the Pensions Regulator’s guidance: Directors and automatic enrolment – do you have duties?.

ii SIPP — from £5.99/month

A Which? Recommended pension option for the self-employed — simple, flexible, and low-cost.

Why was it introduced?

Workplace pension savings had been declining for over a decade. Auto-enrolment was introduced to reverse this trend. By harnessing the power of inertia, it is hoped that more UK workers will save for their retirement.

Over 10 million people have been enrolled in workplace pensions, with opt-out rates remaining low at around 8-9%. This demonstrates that when saving is made simple, most employees participate in pensions.

Auto enrolment applies to all employers. If you start a new business, your AE duties begin immediately upon hiring your first employee.

When do new businesses need to register for auto enrolment?

New employers must comply with auto enrolment as soon as they hire staff. Follow the excellent advice on the Pensions Regulator website to get started.

What are the pension contribution rates?

The cost of implementing auto enrolment depends on your pension provider choice and current internal systems.

Ongoing costs include contributions to staff pensions, which depend on the average salary of the members and the chosen contribution structure.

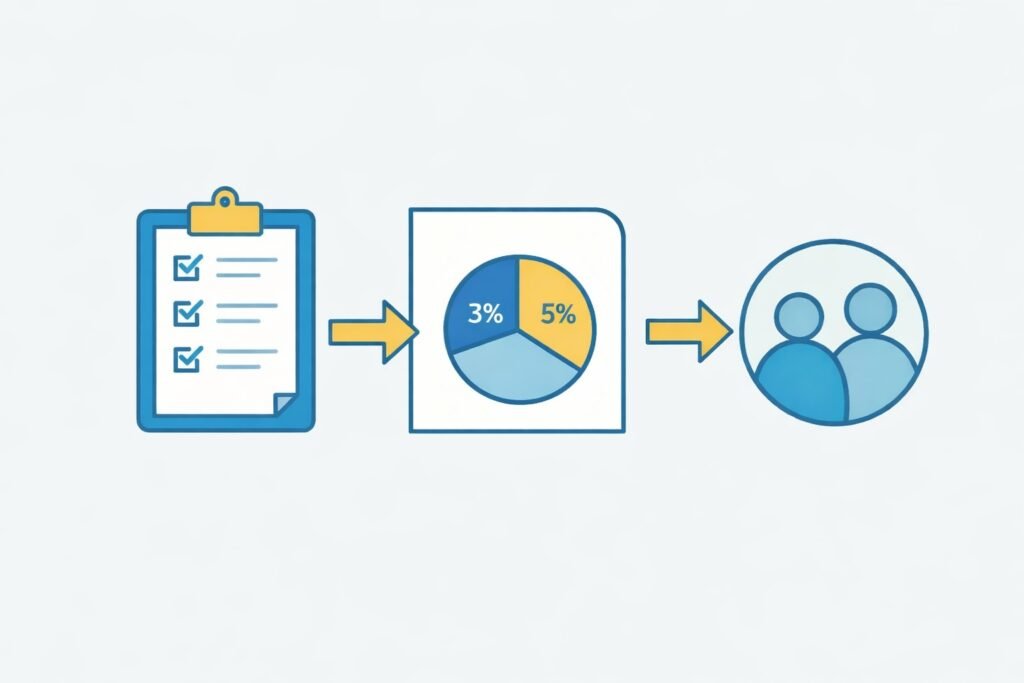

Here are the minimum contribution levels. They have remained unchanged since October 2018:

| Date | Employer minimum contribution (% of qualifying earnings) | Total minimum contribution (% of qualifying earnings) |

|---|---|---|

| Current (since October 2018) | 3% | 8% |

The percentages apply to qualifying earnings (see below). Employers may contribute more, provided they meet the minimum requirement.

Which employees are eligible for auto enrolment?

Employees are eligible if they:

- Staff between 22 and state pension age (currently 66) who earn over £10,000 a year – you must automatically enrol them.

- Staff aged 16 to 74 earning between £6,240 and £10,000 a year – they can choose to join if they want, and you’ll need to chip in contributions if they do.

- Staff earning less than £6,240 a year – they can join a pension scheme, but you don’t have to contribute.

- Staff earning over £10,000 who are either under 22 or over state pension age – they won’t be automatically enrolled, but they can opt in and you’ll need to contribute if they do.

Contributions are calculated on qualifying earnings between the lower level (£6,240) and upper level (£50,270) for the 2025/26 tax year (and carried forward into 2026/27).

The Department for Work and Pensions (DWP) reviews these thresholds annually, but they have remained unchanged for many years.

You can check the latest on the Pensions Regulator site: Earnings thresholds.

Employees can also opt out of a workplace pension scheme, but they must be re-enrolled every three years.

How do you choose a workplace pension scheme?

When you choose a new scheme, review the costs and benefits of each provider and make sure it’s suitable for your business size and goals. Also, be aware that not all providers will take on your company.

Look out for schemes that hold the Pension Quality Mark (PQM), awarded by the National Association of Pension Funds to schemes with strong governance, low charges, and effective communication with members.

The Master Trust Assurance Framework (AAF 02/07) is another useful benchmark for checking pension scheme quality.

What about NEST?

Many employers use NEST because it was set up by the government specifically for automatic enrolment.

It’s uncomplicated to get started, is open to all employers (including small firms), and has clear fees.

If you want a simple, compliant, and uncomplicated solution, learn more on the NEST website.

If you’re unsure, consult an independent financial advisor or your accountant.

Read more on the Pensions Regulator site: Choose a pension scheme for automatic enrolment.

What do you need to keep doing after auto-enrolment?

Once you have set up a workplace scheme, you also need to keep on top of some ongoing tasks, including:

- Make your employers’ contributions regularly and process your employees’ contributions.

- Monitor your employees’ earnings and be aware of the ages of current and new staff members.

- Handly any requests to opt in, join, or opt out of your scheme promptly.

- Keep accurate and up-to-date records of everything

- Remembers that you must re-enrol eligible staff every three years. Even if they’ve opted out in the past!